General

Sri Lanka tax collections up 54-pct in 2023, exceeds revised target, deficit lower

Sri Lanka tax collections higher than revised 2023 target, deficit lower

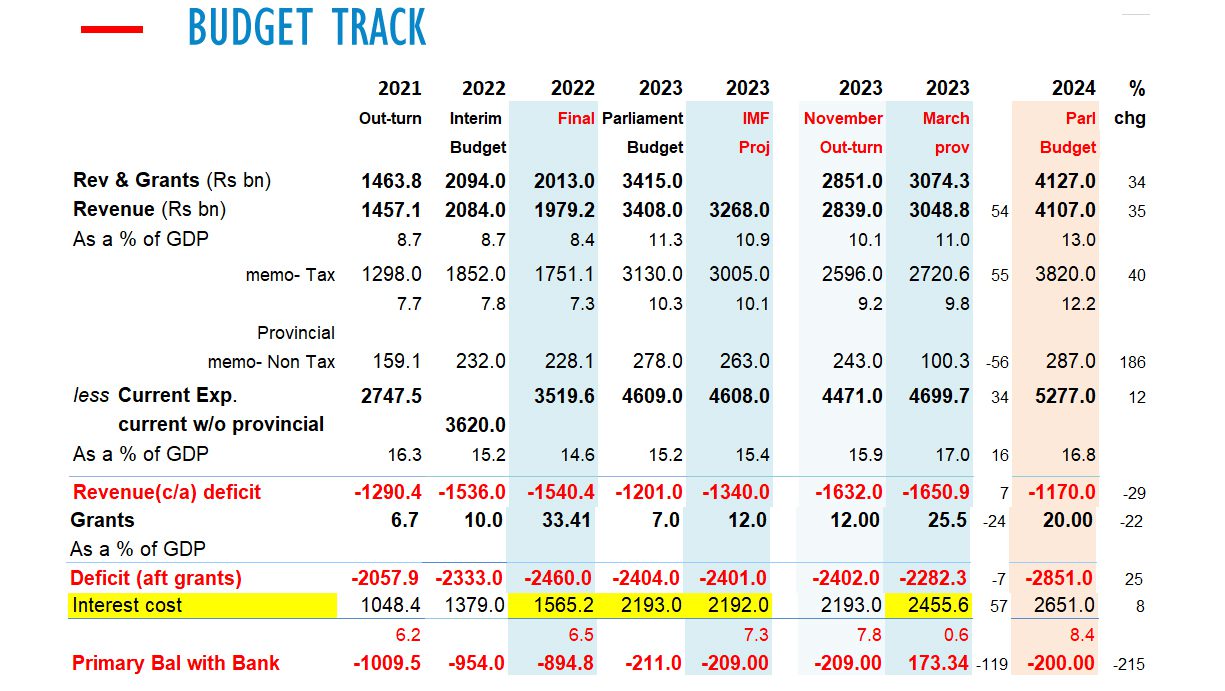

ECONOMYNEXT – Sri Lanka’s tax collections in 2023 have totalled 2,750 billion rupees, up 55 from 2022 and higher than a revised out-turn presented at a November, official data show.

Sri Lanka originally targeted 3,130 billion rupees of tax collections in 2023 or 10.3-pct of gross domestic product despite an economic contraction but with an inflated economy at hikes in rates, while the International Monetary Fund projected only 3,005 billion rupees (10.1-pct of GDP).

In a budget for 2024 presented to parliament in November, the tax target was revised down to 2,596 billion rupees, or 9.2 percent of GDP.

But the actual collections have turned out to be 2,720 billion rupees for 2023, which is 8.9 percent of GDP.

With non tax revenues of 100 billion rupees, lower than expected, total revenues were 3,048.8 billion rupees or 11 percent of GDP, in slightly lower than the 11.3 percent in the original budget but in line with the 10.9 percent IMF projection.

High Nominal Rates and Monetary Instability

Current spending climbed 34 percent to 4,699 billion rupees in 2023, largely driven by interest cost of 2,455 billion rupees, up 57 percent.

In countries without a credible monetary anchor, frequent balance of payments crises and high inflation drive up nominal interest rates as one currency crises follows another and stabilization program come in their wake.

Sri Lanka is operating flexible inflation targeting (trying to target inflation without a clean floating exchange rate), triggering currency crisis as soon as private credit recovers, when inflationary open market operations are deployed to cut rates.

Sri Lanka started to suffer from severe currency deprecation and inflation after 1978 as the country was cut off without a credible anchor after the IMF’s Second Amendment to its articles.

At the time money supply targeting without a clean float was peddled to the country, just as inflation targeting without a clean float has been peddled now, critics say.

Flexible inflation targeting was also combined by macro-economists with potential output targeting (printing money for growth) after the end of a 30-year civil war, leaving the country with rapidly rising foreign debt and eventual default, instead of a peace dividend.

Deficit

The high current spending driven by interest costs, left the government with a revenue deficit (deficit in the current account of the budget), 1,650 billion rupees, higher than a revised target of 1,632 billion rupees and up 7 percent from 2022.

The overall deficit was contained by sharply cutting capital expenditure to 656.9 billion rupees, from 952.9 billion rupees in 2022.

In 2023 most bilateral projects were halted after the country defaulted in 2022.

The overall deficit, after grants of 25.5 billion rupees came in at 2,282 billion rupees or 8.3 percent of GDP, slightly higher than the 7.9 percent of GDP projected in the original budget, and 8.0 percent projected by the IMF.

The deficit was lower than the 10.2 percent recorded in 2022 and also down in absolute terms 2,460 billion rupees.

Primary Surplus

The primary account, (deficit before interest) was a surplus of 173.34 billion rupees.

The International Monetary Fund targets the primary deficit in countries with balance of payments crisis, instead of the overall deficit as steep rate hikes are required to correct currency collapses and kill private credit.

Targeting the primary deficit, reduces the incentive for trigger happy central banks to print money to try and reduce the interest bill and trigger further meltdowns of the economy, which has been put in jeopardy by inflationary rate cuts.

A primary surplus indicates that the country’s interest bill is so bad (usually from monetary instability) that it exceeds the overall budget deficit.

The overall budget deficit is usually contained by cutting capex which is not really required in a country going into a monetary meltdown or hyperinflation after rate cuts.

Sri Lanka has rarely recorded primary surpluses, except in extreme crisis years.

In order to bring down deficits, debt, the economic principle is to run a surplus in the current account, which also requires cutting spending as well as revenue gains and long term monetary and exchange rate stability to bring down interest rates and tax rates.

In the run up to the default Sri Lanka has been operating revenue based fiscal consolidation (avoiding spending cuts and allowing a bloated state to expand further in an unusually statist strategy), and also aiming for primary surpluses, while current account and overall deficits deficits worsened.

Overall deficits generally worsen in stabilization years and can be brought down if macro-economists allow people to work and grow their businesses and personal finances without triggering monetary stability by chasing conflicting anchors or printing money to cut rates.

A current account surplus indicates that all current spending is financed by revenues and there is a little left over for capital spending. (Colombo/Apr27/2024)