General

Sri Lanka, other defaulting nations have widely differing debt indicators: Expert

ECONOMYNEXT – Sri Lanka other recently defaulting nations have widely differing debt indicators, and some other countries survive with even higher levels of debt, a US based analyst has said.

“If you look at the ratio of debt to GDP, the size of the economy the number is very high, mostly because there has been a lot of depreciation, so the debt in dollars keeps growing relative to GDP,” Sergai Lanau, Deputy Chief Economist at Washington based Institute of International Finance said.

“This is sometimes over-emphasized… but this ratio at 120 is a lot.”

He was speaking at a forum organized by the Bar Association of Sri Lanka.

“Just for a reference point about 6 or 7 years ago Italy’s debt was 120 percent GDP, there was a lot of concern in the Euro area and that is a country that has the ECB. So Sri Lanka at 120 is a lot.”

Italy however is in a monetary union with Euro which is a floating exchange rate without anchor conflicts and forex shortages and basic external payment problems.

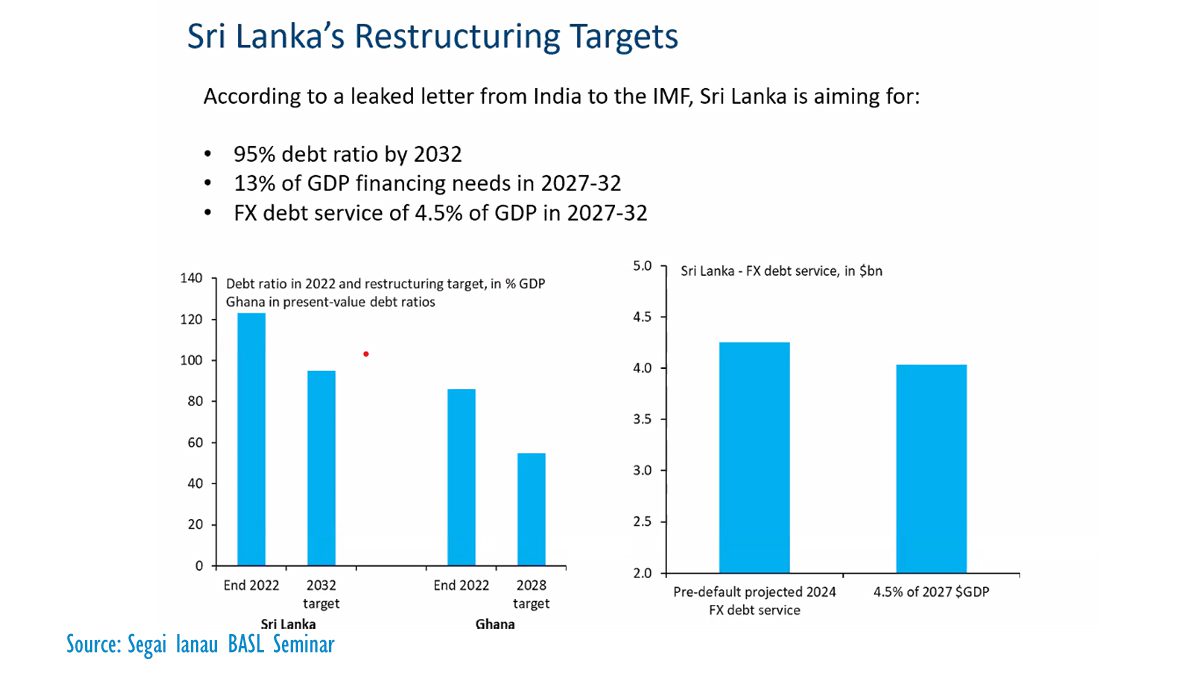

Sri Lanka is trying to bring the ratio down to 95 percent by 2032 under an International Monetary Fund backed program, according to a leaked letter from India.

“Typically for many years there was as lot of emphasis on debt ratios, when people looked at debt restructuring – or at least economists,” Lanau said.

“And that is something that always puzzled bond traders who came from the corporate sector. For them it is all about the flows and gross financing needs.

“The IMF has shifted its focus a lot financing needs over the years and it is a less of a problem now.”

Ghana has defaulted and it is trying to reduce its debt from around 90 percent to below 60 percent by 2028. It is starting at a much lower level and correcting within a shorter period to an even lower level.

Sri Lanka’s debt ratio is high but it “may or may not be a constraint”, he said.

Elephant in the room

A country with a soft pegged central bank (flexible exchange rate or intermediate regime) will see debt rocket each time it suppresses interest rates to target a policy rate and triggers a currency crisis.

Once a currency crisis hits, on one had the domestic currency value of external debt which is denominated in dollars protecting sovereign bond holders, goes up.

Interest rates of domestic debt also have to go up to stop the money printing and halt forex shortages which can widen the overall deficit in the short term.

The currency collapse also kills purchasing power and the real economy slows or contracts.

Once the credibility of the exchange rate has been lost, due to excess money injected the country loses the ability to settle both imports and debt repayment by exchanging domestic money for dollars.

The reserves (savings of past years) are used for current imports and debt repayments more money is injected to sterilize the interventions to maintain the policy rate, reserves collected over several years are run down in a few months.

Falling reserves, a depreciating currency then trigger rating downgrades (usually due to so-called exchange rate of as the first line of defence which saw downgrades in 2018 and 2020 in Sri Lanka) and sovereign bond as yields soar, and market access is lost, triggering a default.

As reserves dwindle further due to holding the policy rate with new money, more downgrades follow.

Countries with flexible exchange rates/flexible inflation targeting with market access can default at virtually any level of debt, critics say.

Market Access

Sri Lanka’s debt to GDP ratio shot up over 100 percent and lost almost all its reserves following a currency crisis in 2000/2001.

But at the time (or in earlier soft-peg crises in 1988/89 and earlier) the country did not have market access and bullet repayment debt.

In Sri Lanka bonds are big part of the country’s debt.

“Once you have lost market access there is virtually no level of gross financing needs that is sustainable,” Lanau said.

Analysts say the once market access has been lost, and the IMF declares that debt is unsustainable, which blocks the World Bank and ADB from giving loans, default is almost certain.

Argentina which has the archetypal soft-pegged Latin America central bank, which sterilizes interventions, strikes zeros off the peso at intervals and get into forex trouble.

“The country got into an IMF program in mid-2018, it was a very optimistic set of IMF targets, policy adjustments,” Lanau said.

“And this IMF program did not work and the situation got critical in August 2019 at which point Argentina defaulted.”

In March 2020 the IMF had presented a debt sustainability analysis where it was expected to to get its debt to 40 percent of GDP by 2030 and foreign exchange debt service to 3 percent of GDP, Lanau said, compared to 4.5 percent for Sri Lanka to make debt sustainable.

Ecuador which had a successful pre-emptive debt re-structuring, had debt levels of around 60 percent when it went talked to bond holders.

It was an ‘easy re-structuring, Lanau said.

It was a “lot about a bunch of maturities coming due in very few years as opposed to a very high debt ratio or a situation that was very unsustainable economically.”

Ecuador however is a dollarized country where its central bank effectively died in the 1990s after the sucre collapsed to 25,000 to the US dollar.

The Central Bank of Ecuador is no longer capable of creating forex shortages or driving the people to starvation and external debt is effectively in domestic currency.

Ecuador’s gross financing needs are now down to around mid single digits, while Sri Lanka’s has shot up to around 30 percent of GDP following the currency collapse.

Ecuador central bank was set up by Edwin Kemmerer, a US money doctor, with a gold peg (no obstinate policy rate) but was corrupted in 1947 by Robert Triffin, a US Keynesian who set up Argentina style central banks in several Latin America countries that frequently defaulted from the 1980s.

Sri Lanka’s central bank was also set up in 1950 by a US money doctor with broadly similar sterilizing powers.

Sri Lanka also started to depreciate the currency from around 1980 without withdrawing inflationary policy (an earlier re-incarnation of first line of defence strategy) triggering strikes, social unrest but no sovereign default due to lack of market access.

Sovereign defaults were mostly absent during the Bretton Woods era even in Latin America when countries maintained their pegs more or less with complementary monetary policy and the IMF also supported external anchors.

However after 1980 when the US tightened policy under Chairman Paul Volcker there were widespread defaults in pegged Latin American countries which did not hike rates in tandem or sterilized interventions (resisted the BOP) trying to operate independent monetary policy.

Now there are a number of market access countries in Africa and Asia with reserve collecting central bank which are trying to operate flexible inflation targeting, another monetary policy which are in conflict with the balance of payments which are ripe for serial currency crises and default.

Clean floating central bank do not use foreign reserves for imports nor collects them. (Colombo/Dec27/2022)